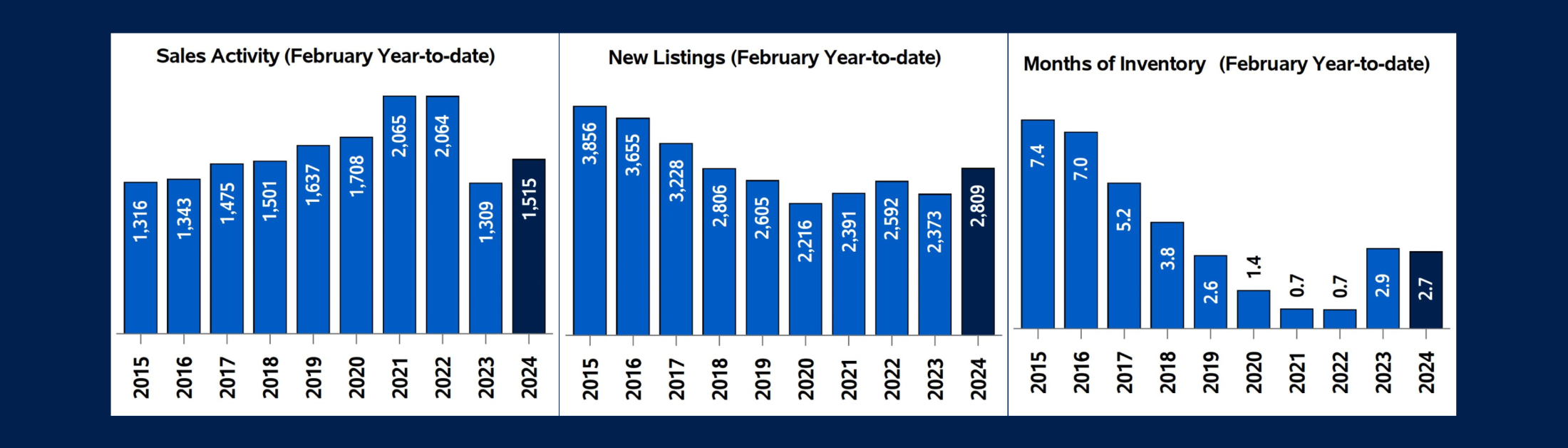

In February 2024, the Ottawa Real Estate Board reported a total of 886 homes sold through the MLS® System, marking a notable 15.2% increase compared to the same month in 2023. However, these sales figures fell 13.8% below the five-year average and 5.7% below the 10-year average for February.

OREB President Curtis Fillier emphasized the robust and active nature of the Ottawa real estate market despite higher prices and stable interest rates. Metrics across various indicators showed positive growth from the previous year, indicating significant activity among both buyers and sellers. Fillier, however, acknowledged the ongoing affordability challenges, with many individuals still unable to participate in the market.

The recent report from the Municipal Property Assessment Corporation (MPAC) revealed a scarcity of communities with homes under $500,000. A decade ago, 74% of Ontario residential properties had a value estimate below $500,000, but this has dwindled to only 19% today. Fillier advocated for impactful measures, such as allowing four residential units on property lots and eliminating exclusionary zoning, to address the lack of affordable housing.

Examining price trends, the MLS® Home Price Index (HPI) showcased a 2.8% increase in the overall composite benchmark price to $628,500 in February 2024 compared to the previous year. The benchmark prices for single-family homes, townhouses/row units, and apartments also exhibited varying gains. The average home price for February 2024 was $651,340, showing a 2% uptick from the same month in 2023. The dollar volume of all home sales surged by 17.5%, reaching $577 million in February 2024.

OREB cautioned against relying solely on the average sale price as an indicator of specific property value changes, emphasizing the variability across different neighbourhoods.

In terms of inventory and new listings, February 2024 witnessed a substantial 29.5% increase in new residential listings, totalling 1,539. Although these new listings were 10.3% above the five-year average, they remained 3.3% below the 10-year average for February. Active residential listings at the end of February 2024 numbered 2,158, marking a 16.3% gain from the same month in 2023. However, they were 59.6% above the five-year average and 17.7% below the 10-year average for February. The months of inventory stood at 2.4, remaining unchanged from February 2023, indicating the time it would take to sell current inventories at the existing rate of sales activity.

.png)