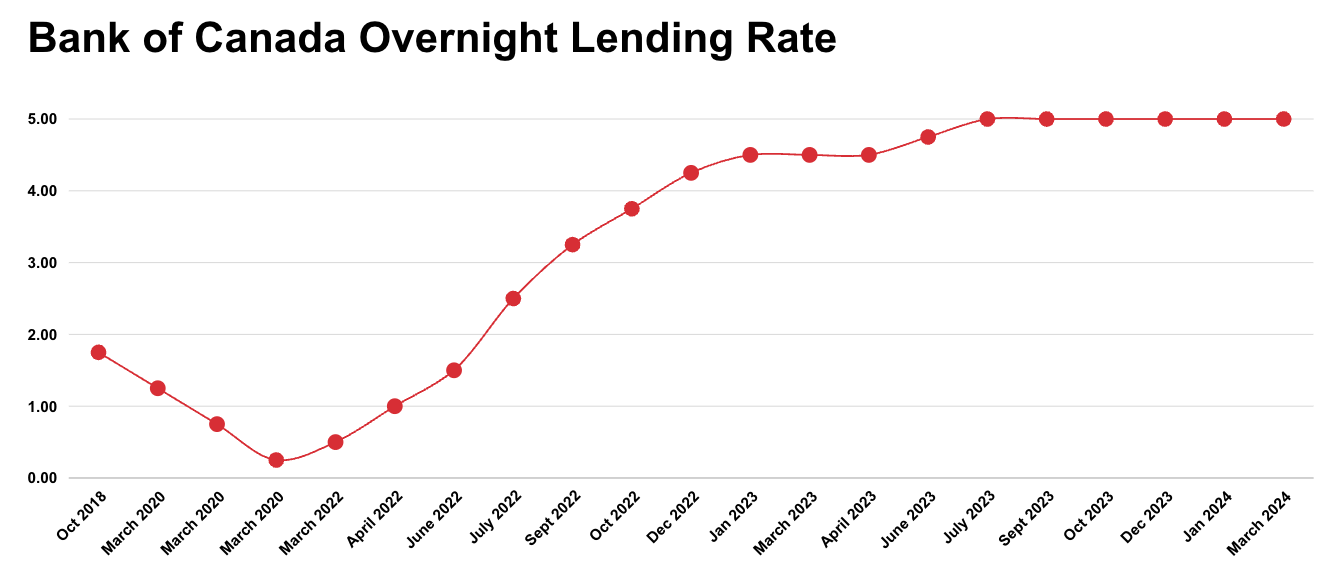

Today, the Bank of Canada lowered its target for the overnight rate to 3.75%, with the Bank Rate set at 4% and the deposit rate at 3.75%. The Bank continues its balance sheet normalization efforts.

Globally, the economy is projected to grow at a steady 3% over the next two years. Growth in the U.S. is anticipated to be stronger than previously expected, while China’s outlook remains cautious. The euro area’s growth has been sluggish but is expected to improve modestly next year. Inflation in advanced economies has decreased recently, aligning with central bank targets. Since July, global financial conditions have eased, partly due to expectations of lower policy interest rates. Additionally, global oil prices are roughly $10 lower than projected in the July Monetary Policy Report (MPR).

In Canada, economic growth was around 2% in the first half of the year, with an anticipated 1.75% growth in the second half. While overall consumption has grown, it has decreased on a per-person basis. Exports have seen a boost from the opening of the Trans Mountain Expansion pipeline. The labor market remains subdued, with the unemployment rate at 6.5% as of September. Population growth continues to expand the labor force, but hiring has been moderate, impacting young people and newcomers the most. Wage growth remains high compared to productivity growth, indicating excess supply in the economy.

Looking ahead, GDP growth is expected to strengthen gradually as lower interest rates support economic activity. A modest increase in consumer spending per capita, along with slower population growth, is expected to drive this recovery. Residential investment is projected to rise, fueled by strong housing demand, while business investment should pick up as overall demand grows. Exports are likely to stay robust, supported by strong U.S. demand.

The Bank forecasts GDP growth of 1.2% in 2024, 2.1% in 2025, and 2.3% in 2026. As the economy gains momentum, the excess supply will gradually be absorbed.

Consumer Price Index (CPI) inflation has dropped notably from 2.7% in June to 1.6% in September. While inflation in shelter costs remains high, it has begun to ease. Excess supply in the broader economy has lowered the prices of many goods and services, and the recent drop in global oil prices has driven down gasoline costs. These factors have collectively brought inflation down. The Bank’s core inflation measures are now below 2.5%. With inflation pressures no longer widespread, expectations from businesses and consumers have largely stabilized.

The Bank anticipates that inflation will hover around its target range throughout the forecast period. The upward pressure from shelter and services costs is expected to diminish, while downward pressures should ease as the economy absorbs the current excess supply.

With inflation nearing the 2% target, the Governing Council has decided to reduce the policy rate by 50 basis points to bolster economic growth and maintain inflation around the mid-point of the 1% to 3% target range. If the economy aligns with the Bank's forecast, additional rate cuts are anticipated. However, the timing and pace of any future reductions will depend on economic data and its implications for inflation. Decisions will be made on a meeting-by-meeting basis. The Bank remains dedicated to maintaining price stability for Canadians, keeping inflation close to the 2% target.

Source: bankofcanada.ca

.png)