In recent years, the Canadian housing market has experienced significant disruptions. A global pandemic, surging interest rates, and economic challenges caused the market to deviate from typical patterns. However, 2025 is anticipated to see a return to conditions more aligned with long-term historical trends.

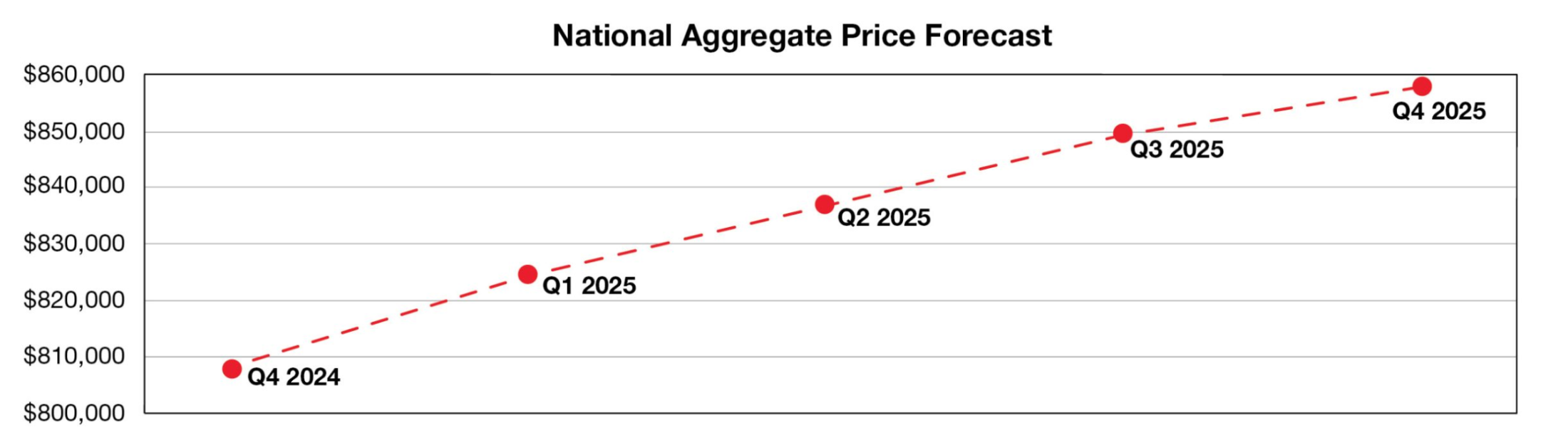

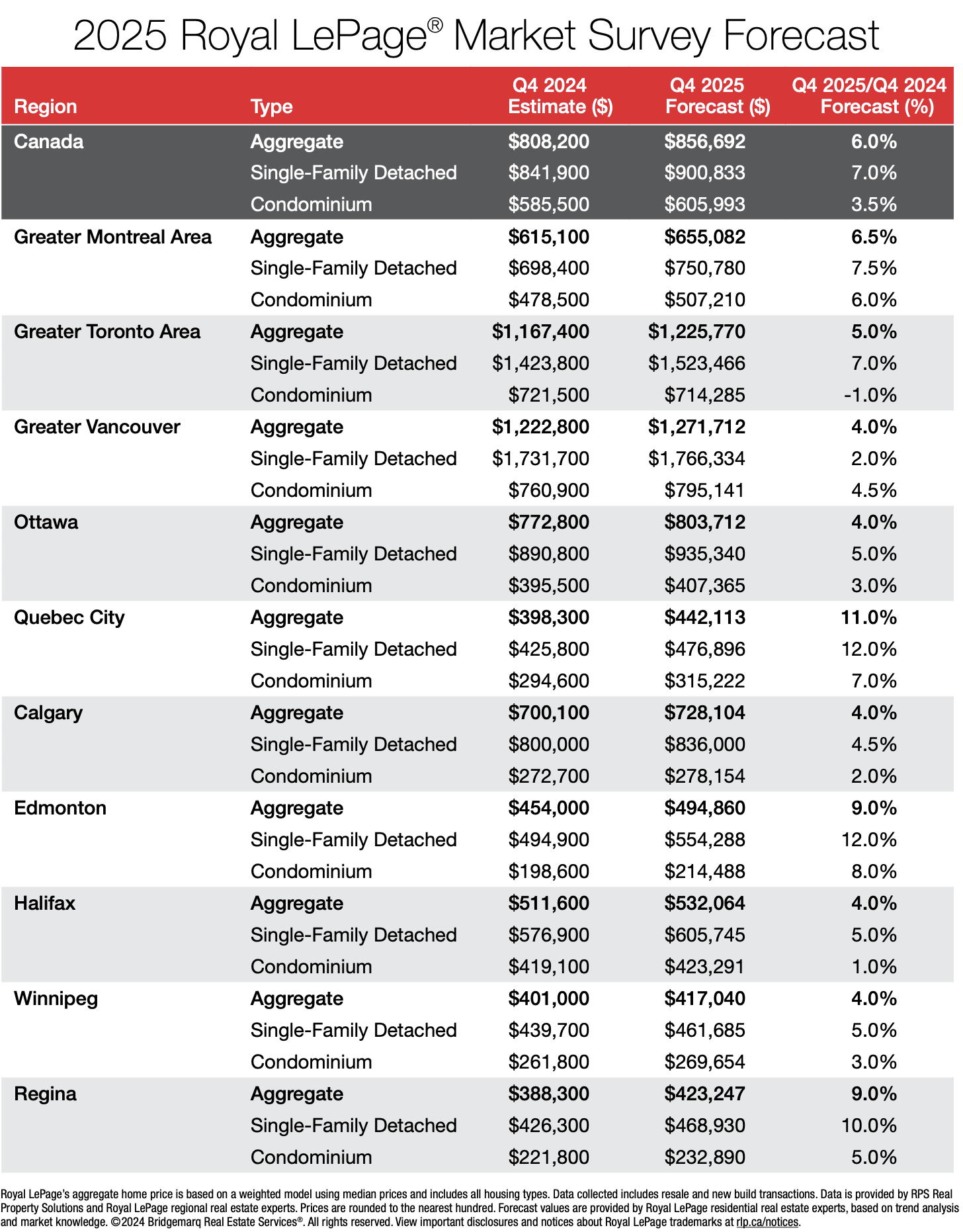

The Royal LePage Market Survey Forecast projects that the aggregate price of a home in Canada will rise by 6.0% year-over-year, reaching $856,692 in the fourth quarter of 2025. The median price of a single-family detached home is expected to grow by 7.0% to $900,833, while condominiums are forecasted to see a 3.5% increase, reaching $605,993.

“After several years of unusual volatility in the real estate market, key indicators point to a return to stability in 2025. The backlog of willing and able buyers continues to grow, and upcoming changes to mortgage lending rules will further enhance Canadians’ borrowing power,” said Phil Soper, president and chief executive officer, Royal LePage. “Most notably, the Bank of Canada’s shift from ‘inflation fighter’ to ‘economy booster’ has taken time to influence buyer behaviour. We saw a marked increase in market activity at the start of the fourth quarter, following the Bank of Canada’s 50-basis-point rate cut. Buyers now believe home prices have hit bottom and are eager to act before competition intensifies.”

New Lending Rules to Enhance Borrowing Power

New lending regulations taking effect this month will provide improved accessibility for first-time buyers and existing homeowners. Starting December 15th, eligibility for 30-year amortizations on insured mortgages will expand to include all first-time buyers and purchasers of new construction homes, an increase from the current 25-year limit. Additionally, the mortgage insurance cap will rise from $1 million to $1.5 million, enabling buyers with less than a 20% down payment to consider higher-value properties. These changes will be especially impactful in Canada’s most expensive real estate markets, where average home prices often exceed $1 million.

“Improved lending conditions, combined with declining interest rates, will unlock new housing opportunities for many Canadians in the new year. First-time buyers will be the primary beneficiaries of these initiatives, as their ability to borrow more for less with a smaller down payment will help bring them closer to their first home purchase,” said Soper. “We believe the return of buyers to the market will encourage builders and trigger a wave of new supply, which is very much needed.

“Addressing Canada’s critical housing shortage must remain a top priority for policymakers at every level of government. With our population growing rapidly through both natural increases and immigration, it is essential to stay focused on supporting the development of new homes if we hope to address housing affordability, be it for purchase or rent.”

Shifting Political Landscapes and Potential Housing Impacts

The year 2025 is expected to bring political changes in both Canada and the United States, with potential implications for the housing market. In Canada, a federal election may introduce new housing policies that could temporarily influence market activity in the latter half of the year.

“With an election approaching in Ottawa and a new administration preparing to take office in Washington, the housing market faces potential disruptions. Here at home, a federal election will see new housing policies that may temporarily impact market activity in the second half of 2025,” said Soper. “Meanwhile, south of the border, the incoming Trump administration’s trade policies and broader economic agenda have the potential to create ripple effects for Canada’s economy and housing market. While these impacts may take time to unfold, they could eventually affect consumer confidence and market dynamics on both sides of the border.”

Highlights from the 2025 Forecast

Greater Montreal Area is expected to lead with aggregate home price growth of 6.5%, outpacing Greater Toronto (5.0%) and Vancouver (4.0%).

Quebec City is forecasted to see the largest increase among major regions, with an 11.0% rise in aggregate home prices, followed by Edmonton and Regina at 9.0%.

Calgary, along with Ottawa, Halifax, and Winnipeg, is projected to experience a moderate 4.0% home price increase, following significant appreciation over the last two years.

The median price of a condominium in the Greater Toronto Area is anticipated to decline by 1.0%, reflecting the addition of thousands of new units to an already surplus supply.

.png)