The Bank of Canada has held its target overnight rate steady at 2.75%, with the Bank Rate set at 3.00% and the deposit rate at 2.70%.

Since the April Monetary Policy Report, the United States has continued to adjust various tariffs, with both the U.S. and China stepping back from earlier aggressive trade measures. Bilateral trade negotiations have resumed with several countries, but outcomes remain highly uncertain. “Tariff rates are well above their levels at the beginning of 2025, and new trade actions are still being threatened. Uncertainty remains high.”

The global economy has shown some resilience, though this is partially due to businesses advancing activity in anticipation of future tariffs. In the U.S., consumer demand stayed solid, though a rise in imports caused a dip in Q1 GDP. Inflation has edged down but still sits above 2%, and the full impact of tariffs on prices has not yet been realized. In Europe, growth has been export-driven, and defence spending is on the rise. China, meanwhile, is experiencing a slowdown as earlier fiscal measures wear off, and its exports to the U.S. are being hindered by steep tariffs. Following April’s market volatility, most risk assets have rebounded and volatility has calmed—though markets remain sensitive to U.S. policy changes. Oil prices have varied but are relatively stable compared to April levels.

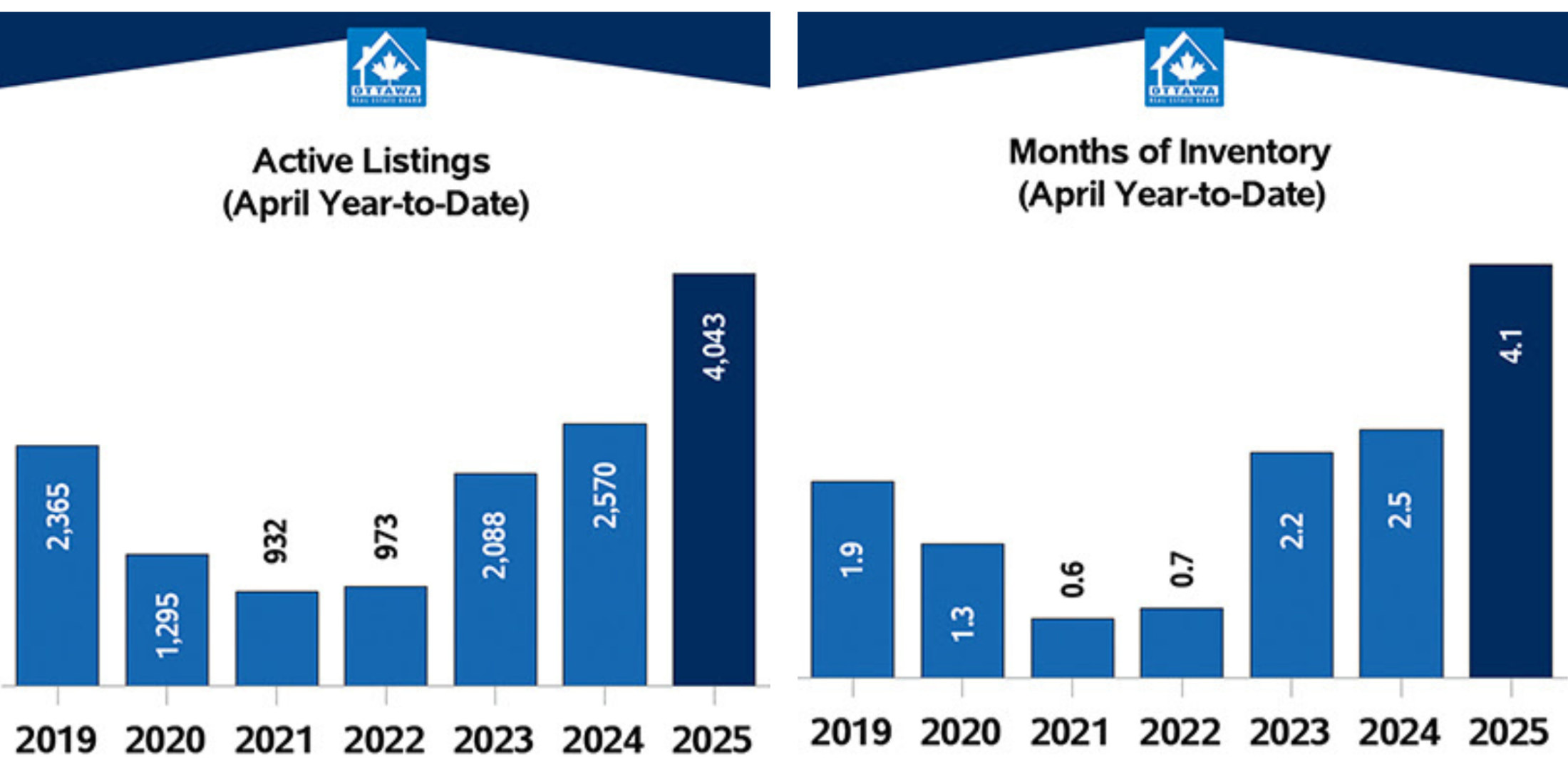

In Canada, Q1 GDP growth reached 2.2%, slightly exceeding the Bank’s forecast. The main drivers were advanced exports to the U.S. and higher inventories, though final domestic demand remained flat. Stronger-than-expected spending on machinery and equipment supported business investment. Consumer spending slowed from Q4 but remained positive, even amid a steep drop in confidence. Housing activity declined, primarily due to a significant drop in resale transactions. Government spending also decreased. The labour market has weakened, particularly in trade-reliant industries, with the unemployment rate now at 6.9%. Looking ahead, economic momentum is expected to slow further in Q2 as earlier gains from exports and inventories fade, and domestic demand stays weak.

CPI inflation eased to 1.7% in April, largely due to the removal of the federal carbon tax, which reduced overall inflation by 0.6 percentage points. “Excluding taxes, inflation rose 2.3% in April, slightly stronger than the Bank had expected.” Key measures of core and underlying inflation also ticked higher. Surveys show that many households expect tariffs to push prices up, and a growing number of businesses intend to pass those costs along. “The Bank will be watching all these indicators closely to gauge how inflationary pressures are evolving.”

Given the ongoing uncertainty around U.S. trade policy, a soft but not sharply declining Canadian economy, and stronger-than-expected inflation data, “Governing Council decided to hold the policy rate as we gain more information on US trade policy and its impacts. We will continue to assess the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs.”

“Governing Council is proceeding carefully, with particular attention to the risks and uncertainties facing the Canadian economy.” These risks include how U.S. tariffs impact demand for Canadian exports, the potential ripple effects on business investment, employment, and household spending, and how quickly businesses pass rising costs on to consumers. Inflation expectations will also remain under scrutiny.

“We are focused on ensuring that Canadians continue to have confidence in price stability through this period of global upheaval. We will support economic growth while ensuring inflation remains well controlled.”

.png)